One of the primary decisions involved in moving is deciding when is the best time to make a move. Because the market is dynamic, it is difficult to project exactly how much prices may go up (or down!).

One of the primary decisions involved in moving is deciding when is the best time to make a move. Because the market is dynamic, it is difficult to project exactly how much prices may go up (or down!).

Click Here to Download "How to Shop for a Mortgage"

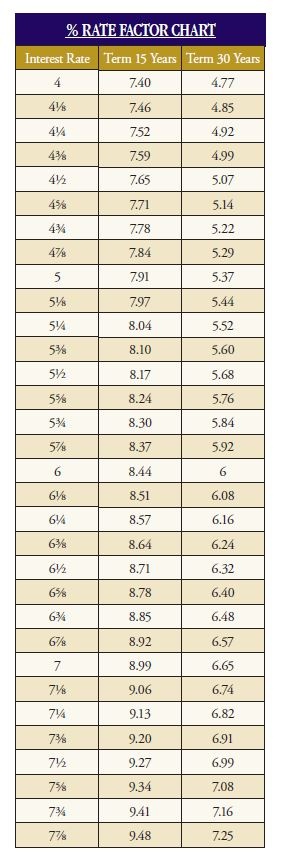

Another important thing to consider is the impact that an increasing interest rate will have on your monthly payment, as it plays a more significant factor than does the sales price.

Use the factor chart to determine what the potential cost of a higher interest rate may actually be.

{kind=link}

Example: a 30 year loan at 4% interest is $1,500 P & I per month, or a mortgage of $314,465. The same loan at 5% & the same payment reduces the mortgage to $279,329, or a little bit over $35,000 in buying power!

Desired monthly P & I _______ ÷ factor _______=

$ × 1,000 = $ ______________(loan amount)

The Cost of Money

Negotiating often involves a balance between emotion & logic. The heart wants what the heart wants, & buyers often worry about justifying a decision that they want to make. We have found it helpful to analyze counter offers (& even initial purchase offers) in terms of the cost of money… & breaking down costs into a daily amount.

Example: $5,000 counter offer at 4% for 30 years is less than 80¢ a day!

To calculate the monthly cost of money, multiply the amount borrowed (divided by 1,000) by the factor for the interest rate & loan duration.

$ needed _______ ÷ 1,000 = _______ × factor of _______ =

$ _______ month P & I ÷ 30 days = $ per day

Are you thinking about starting the home buying process? Talking to a local lender is a great first step! Contact Ginny Phillips or Jim Baldasare, with Atlantic Bay Mortgage Group, at ginnyphillips@atlanticbay.com and jimbaldasare@atlanticbay.com and they can help get you started.